Consultation has opened on the Modern Slavery Bill (Bill), which passed its first reading with cross-party support. With both major parties committed to advancing the Bill (potentially this year, followed by a six-month phase-in period) large organisations should start considering how the regime will affect them and whether to submit on the Bill. Submissions close on 28 May 2026.

Key features of the Bill

"Modern slavery" under the Bill broadly encompasses slavery, trafficking, forced or exploitative labour, the worst forms of child labour, sexual exploitation, debt bondage or serfdom, servitude and coerced marriage or civil union.

The Bill aims to reduce the prevalence of modern slavery, increase public awareness and improve support for victims. To achieve this, it requires "reporting entities" to report annually on matters relating to modern slavery within their operations and supply chains.

"Reporting entities" will have to prepare and publish a modern slavery statement

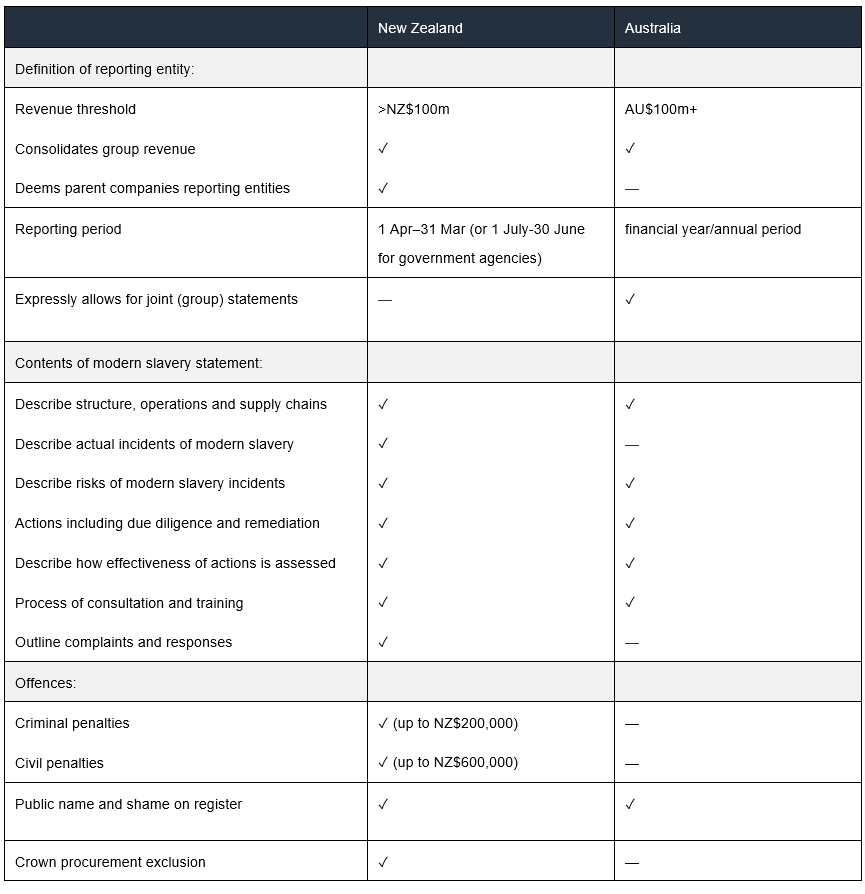

The Bill applies to organisations with total revenue over $100m during the 12-month period from 1 April to 31 March (reporting period). To fall in scope, the entity must be established, managed or controlled in New Zealand, or have carried on business in New Zealand as an overseas company during the reporting period. The definition of "entity" is wide and includes companies, trusts, partnerships, societies, and public sector entities such as Crown departments and local authorities.

Each reporting entity must prepare and publish an annual modern slavery statement covering its operations and supply chain.

Companies forming part of a group

The regime also captures parent companies of reporting entities, and it's not clear whether this would include an overseas parent. A parent company’s total revenue includes the consolidated revenue of all entities it controls, so even where individual New Zealand subsidiaries do not meet the $100m threshold, their combined revenue may bring the parent within scope. Who will be required to report in the context of specific group arrangements, and in the context of multinational companies, will therefore need careful consideration.

Consequences of non-compliance

The Bill includes significantly more severe penalties than its Australian equivalent, which currently has no criminal or civil penalties for non-compliance. The Bill proposes that:

- Failure to submit or publish a modern slavery statement will be a criminal offence carrying a fine of up to $200,000. Pecuniary penalties of up to $600,000 may also be ordered. Providing false or misleading information in a statement would similarly carry a fine of up to $200,000.

- Non-compliant entities will also be publicly named on the register and subject to a mandatory Crown procurement exclusion, preventing them from receiving any funds from the Crown seemingly indefinitely. This is a notably onerous consequence given that it may be triggered by an administrative or procedural failure, rather than any actual instance of modern slavery.

- Directors and individuals involved in the management of the reporting entity could be held personally liable for offences committed by the entity, where those individuals have the requisite level of involvement.

Alignment with Australia

The reporting requirements in the Bill are broadly modelled on its Australian counterpart. However, there are differences in the detail of those requirements, and additional material proposed for New Zealand statements. These include requirements to report on incidents of modern slavery, and outline complaints and associated responses (which have been considered in Australia but not yet implemented).

Trans-Tasman businesses should also note that the reporting periods under the Australian and New Zealand regimes do not currently align (and the potential mismatch in New Zealand with an organisation's financial year makes it harder to apply the revenue threshold). Additionally, the New Zealand Bill is silent on whether related organisations can file together, something Australia permits. Allowing businesses to report based on their financial years (as is the case in Australia), and expressly permitting the filing of joint or group statements, would be straightforward fixes for the Select Committee to consider.

The table below compares key aspects of the Australian and proposed New Zealand regimes at a high level:

Time to get ready

Preparing a modern slavery statement will require due diligence, risk assessments and input from across an organisation, its suppliers and other companies in the group. Impacted organisations will also need new policies, training and accompanying change management, for example by updating template supplier agreements. All of this takes time and introduces ongoing compliance burden.

If your organisation is likely to be caught by the regime or impacted because it is a supplier to a reporting entity, it is important to start thinking now about how the regime will impact you at a practical level. To the extent you identify pain-points, submitting on the Bill during the current consultation period will be valuable. Consider, for example:

- Are fixed reporting dates suitable, or should entities be permitted to align with their own financial balance dates?

- How will the definition of reporting entity apply in the context of your particular structure, and should there be express provision for joint group statements?

- Is the $100m annual revenue threshold appropriate, given that most businesses' revenue fluctuates year-to-year? For context, some comparable reporting obligations (such as large companies' financial reporting requirements in the Companies Act and Financial Reporting Act) require an organisation to meet the threshold for two consecutive periods before qualifying. Might that be appropriate here?

- When applied to your organisational structure and supply chain, is the list of information to be included in a statement clear and achievable in practice? Examples of how organisations have approached similar requirements in Australia (available at Modern Slavery Statements Register) may be a useful practical reference point.

- Are the penalties proportionate? In particular, a mandatory and perpetual Crown procurement exclusion is an unusual and significant potential consequence.

If you would like assistance with submissions, or help understanding how the Bill may impact your organisation, please get in touch.

This article was co-authored by Hugo Young (law clerk) and Kayla Strong (summer clerk).